What day is best for you?

<

>

- Sun

- Mon

- Tue

- Wed

- Thu

- Fri

- Sat

What time works?

30 minutes meeting

Asia/Kolkata Time

Almost there!

IST

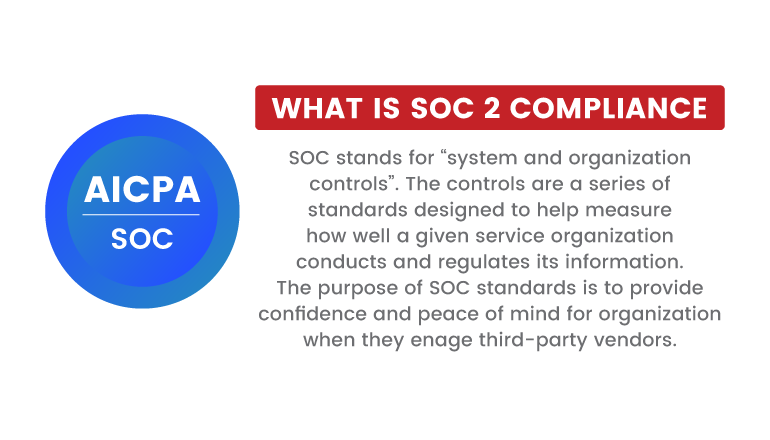

SSAE 18, is an attestation standard issued by the Auditing Standards Board (ASB) of the American Institute of Certified Public Accountants (AICPA). SSAE18 is an attestation standard geared towards addressing engagements conducted by ‘Service Auditors’ (or) ‘Practitioners’ on service organizations for purposes of reporting on the design of controls and their operating effectiveness.

Cybersecurity starts from proper awareness. Briskinfosec BINT LAB cybersecurity researchers continuously put extraordinary effort to help you to realise cybersecurity better and faster. Just download the Threatsploit Adversary report.

Your window into the evolving threat landscape, offering insights and intelligence to protect against emerging cyber dangers.

SOC 1 Reports: Reporting on controls relevant to internal controls over financial reporting (ICFR) and reporting is conducted in accordance with Statement on Standards for Attestation Engagements - SSAE as per the standards of SSAE 18 audit guide.

SOC 2 Reports: Reporting on controls relevant to security, availability, processing integrity, confidentiality, or privacy. SOC 2 reporting are conducted in accordance with AT Section 101 and will utilize an audit guide titled Reports on Controls at a Service Organization over Security, Availability, Processing Integrity, Confidentiality, or Privacy

Type 1 report is technically known as a "Report on Management's Description of a Service Organization's System and the Suitability of the Design of Controls", or simply known as a SOC 1 SSAE 18 Type 1 report.

Type 2 report, it is technically known as a "Report on Management's Description of a Service Organization's System and the Suitability of the Design and Operating Effectiveness of Controls", or simply known as a SOC 1 SSAE 18 Type 2 report.

Once the scope is determined, a service organization like Briskinfosec may decide to assess the gap and existing controls in place and to determine if they satisfy management’s control objectives are in place.

Whether they meet the control objectives and all are in order

In case if controls are not adequate a remediation effort will be designed / developed to take counter measures and to fix the gaps.

As with any compliance enforcement, violating the CCPA comes with a price tag. Under Section 17206 of the California Business and Professions Code penalties are $2,500 for an unintentional violation, and $7,500 for intentional violations.

The new privacy law will allow individuals to recover between $100 and $750 per incident—or greater if there’s solid evidence that damages exceed $750.

Following sequence of steps occur during the remediation phase:

Remediation services would be provided and efforts are tracked and adequacy of controls established in order to close and to fix the gaps.

Service provider will draft a system description that identifies processes and controls that deliver the services within the scope of the engagement. This description is the basis of the auditor’s opinion and will be included in the final report.

Following sequence of steps occur during the remediation phaseAfter remediation services performed and identified control gaps including the control description.

The successful result of these procedures is the issuance of a Type 1 SOC report with Service Auditors Opinion as of a specific date.

It’s a kind of belief and trust from your valuable Customers; who have received services from your organization, for the internal controls maintained and implemented.

Because of the changes from SSAE 16 to SSAE 18, your service organization can benefit in the following ways:

Provide a broad-based Centric Approach, enhanced reporting of your control system.

Full Assurance for your customers on the internal control Audits affecting their financial reporting are timely and accurate in order to stay in compliance with company policies and government regulations.

SSAE 18 engagements identify key areas for improvement that can ultimately help to reduce risk, decrease the frequency of irregularities, and minimize chances of fraud.

What Does CPA Reporting Mean - For SSAE18 physical security compliance?

When an independent CPA reports about your high compliance to SSAE, you’d be able to assure your clients that you have high level of security that would not be compromised.This is because means that you have set the right hierarchical responsibility for access to your premises and most importantly that you work with partners that don’t take data security lightly.

While the SSAE 16 was specific to SOC 1 audits, SSAE 18 is an umbrella standard that applies to most types of attestation engagements, clarifying and formalizing requirements to enhance their reporting potential.

SSAE 18 features significant changes in the following areas:

Vendor management

Risk assessment

Complementary subservice organization controls

Data validation

What is SSAE 18 Compliance in Access Control?

The SSAE 18 guidance primarily clarifies existing auditing standards. It is also intended to reduce instances of duplication within similar standards that cover Examinations, Reviews and Agreed Procedure engagements.

As of May 1, these engagements – specifically, SSAE nos. 10-17 – will fall under the SSAE 18

This is why SSAE 18 access control compliance for today’s service companies entails more than just physical requirements.

Celebrating our achievements and collaborations, shaping a future of excellence.

Get more answers to your questions in our Learning Services FAQ

Expert guidance, tailored solutions- your direct path to insightful, precise answers.

Book an Appointment